Throughout the spring, I’ve been co-leading a small group at church for some of our youth based on Crown Financial’s Discovering God’s Way of Handling Money. It’s been such a fun semester with these inquisitive, intelligent students and it’s been fun to share one of my passions (personal finance) with them.

The last two Wednesdays, we’ve talked about investing. We specifically talked about investing in stocks, because that’s what most people think of when they hear the word “investing.”

I’ve been investing in stocks for about 25 years. (Maybe a more accurate way of saying that is: I have been investing in stocks for about 25 years, many of those under my dad’s wise tutelage.) My dad has helped me invest in stocks from a very early age and I’ve learned a few things since my very first shares (Campbell’s Soup, FTW). I thought I’d share with you what I shared with them.

So here are 10 lessons I’ve learned about investing. Many of these are about more than just investing and could be categorized as life advice. I think that’s because life has informed my investing and investing has informed my life. So, without further adieu, here are 10 lessons I’ve learned from from investing.

And, as a preventative measure so I don’t get sued: This is not financial advice. Each financial situation is different and not all of this will be applicable for every person. These are just things I’ve learned from my own experience. So if you lose money, it’s not my fault. Don’t blame me. Or sue me. Please.

1. Know Your Why

Before any money goes into the market, you have to know your why. Why are you wanting to invest money? When you know your why, you’ll know where and how to invest your money and have the fortitude to withstand market bumps and drops.

For example, I’ve been saving up for the last many years to buy a new-to-me vehicle. I hope to purchase one this year. Because I’m working with such a short time-horizon, I’ve chosen to put the money I’ve saved for a vehicle in a High-Yield Savings Account (HYSA). The 5% I earn in the HYSA is less than the average 8-10% annualized return the stock market delivers, but I don’t want to watch that money fluctuate the way a stock does.

However, for my retirement investments, I’m putting my money in stocks (which I’ll talk about more later). The huge drops that can happen in the stock market can be gut-wrenching, but because I don’t need the money anytime soon, I know that these drops too shall pass.

Additionally, knowing your why helps you have the fortitude needed to withstand the turbulence of financial markets. Take, for example, the 2008 crash. If you blissfully put money into the stock market in 2007 just because everybody said that you should invest in stocks, then by March 2009, you’d have lost 54% of your money. If in March you thought, “Why am I even doing this?” and pulled your money out, you’d have been better off just keeping all that money stashed under your mattress. Having the big picture in mind (your “why”) helps you fight the temptation to bail when things are bad.

In investing (and in life), knowing your why helps keep you focused on the end goal.

2. “Easy choices, hard life. Hard choices, easy life.”

I first heard this quote on one of my favorite podcasts, ChooseFI. While it’s not universally true, it’s a great guiding light for investing.

If you are willing to make hard choices now (living beneath your means, investing in retirement funds, etc.) you’ll have a much easier life in the future. But if you make easy choices now (rack up credit card debt, spend all of your money, etc.), it will make life much harder in the future.

Which leads me to #3…

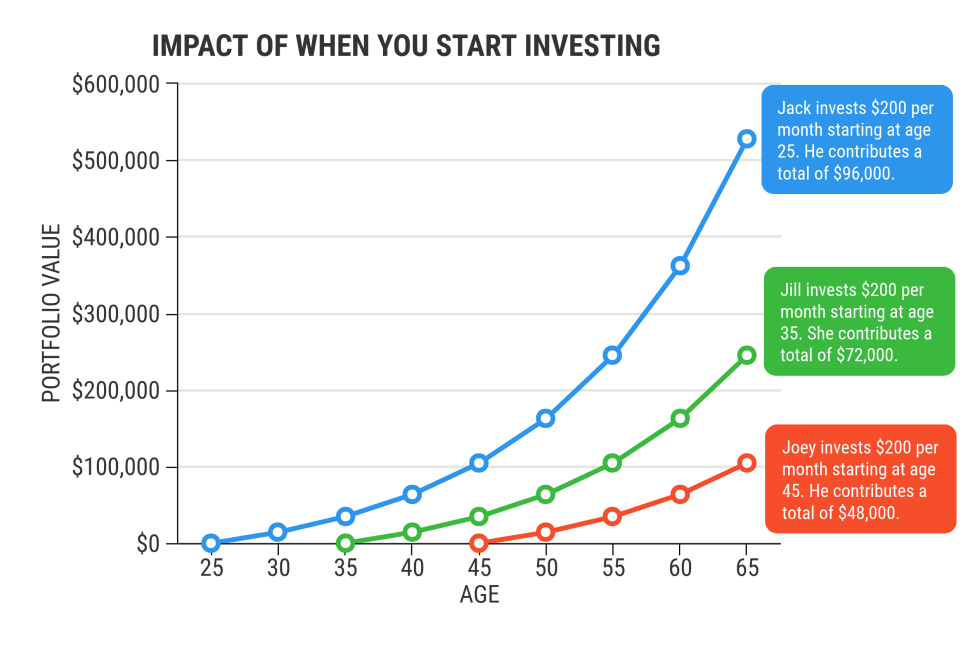

3. Start early and/or start now.

My dad is incredibly wise with money and I’m fortunate that he shared much of his wisdom with me.

Because of my dad’s financial wisdom, one of his friends (we’ll call him Jim) asked my dad to sit down with his adult son (we’ll call him Sam) and talk with Sam about finances. My dad took Sam out to lunch and shared his wisdom. After Sam told Jim how impactful the lunch was, Jim asked if my dad could impart the same wisdom to him. My dad told Jim that he didn’t have anything to share. Sam—who was in his 20s at the time—was told to invest now and watch his returns grow. For Jim—who was in the latter half of his career—the same advice wasn’t as true.

Even though I was in grade school, that moment stuck with me. I realized that the earlier I started, the easier it would be for me to have enough money when I wanted and needed to retire.

US News and World Reports shows how the magic of compound interest and starting early makes a world of a difference in retirement:

But maybe you’re like Jim and in the latter half of retirement. All’s not lost for you. One of my favorite quotes is a Chinese proverb: “The best time to plant a tree was 20 years ago. The second best time is now.”

Start early. And if you can’t start early, start now.

4. Simplicity = success

Another way to reframe this would be “Hard to understand = easy to lose money.”

Investing can be overly complicated. In fact, many people make money by making finances more complicated than it needs to be.

For example, if an investment firm makes you feel like investing is important but that you’ll never understand how to invest, then being charged 2% for them to handle all of your investing seems like a bargain. Confusion and complication helps that investment firm make money.

When most people think about investing in stocks, they think about investing in individual stocks (“stock picking,” as some people like to refer to it as). But there are other, safer, and less time-consuming ways to invest in stocks. In my opinion, the simplest way to invest (and one of the most surefire ways to make a lot of money in the long run) is to put your money in a low-cost broad-based index fund such as VTSAX (which invests in all 3,000+ publicly-traded companies on the New York Stock Exchange and Nasdaq). Funds like VTSAX will charge you extremely low fees (see #8) and being in such a broad index allows for maximum diversity in stocks. Plus, I believe that you’re able to make more money more consistently through investing in low-cost index funds. J.L. Collins’ The Simple Path to Wealth and the ChooseFI podcast go into much greater detail as to why I hold that belief.

In full transparency, I invest in some individual stocks. But they make up less than 50% of my stock portfolio (and I’m working to get it down to only 10% of my portfolio). I enjoy researching stocks. If you don’t, then individual stock investing isn’t for you.

Our culture tells us that simplicity is bad and complexity means we’re doing something right. It’s okay to make the simple choice and just be happy making a lot of money and not spending a lot of time doing it.

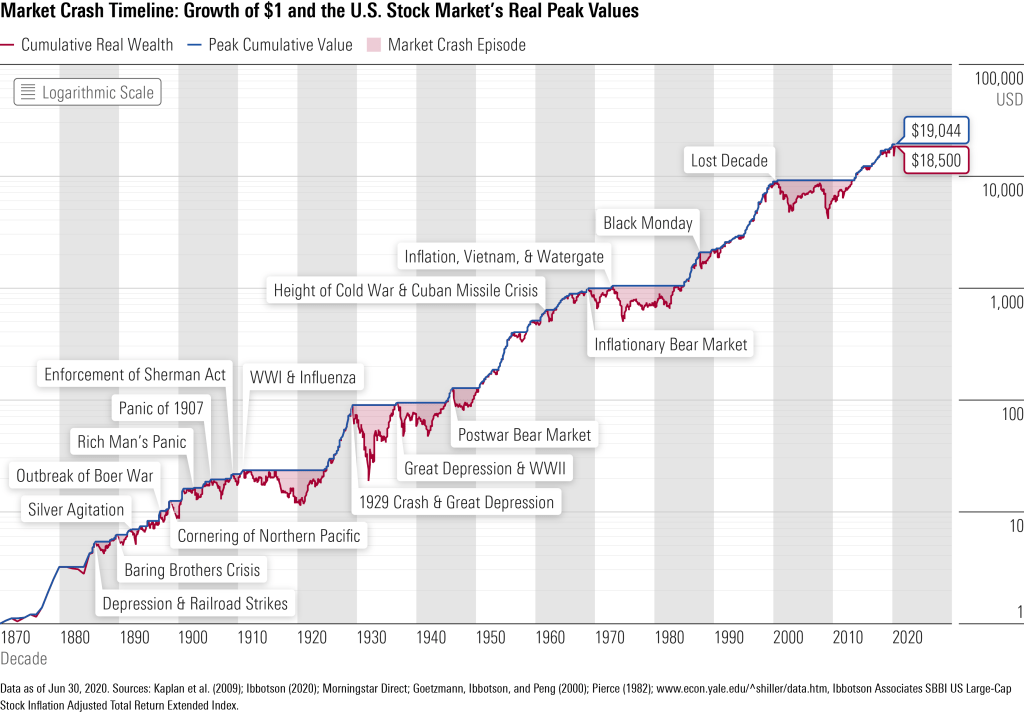

5. The Stock Market Always Goes Up*

I’m stealing this one from the title of Brian Feroldi’s book Why Does the Stock Market Go Up? When you look at the history of the stock market, it’s pretty easy to agree that the stock market does go up:

There’s an asterisk on this one because (as anyone who’s ever heard the news knows) the stock market doesn’t always go up. In fact, it fluctuates. A LOT. But if you’re willing to wait long enough, history tells us that the stock market will go back up. In fact, in the entire history of the US stock market, if you held stocks for more than 18 years, there’s never been a time in history when you’ve lost money. And typically, you have to wait much less than 18 years to make money.

6. Time in the market > Timing the market

This is another insight I’ve learned from the podcast ChooseFI (I’m telling y’all, it’s amazing).

When people try to invest in individual stocks, they think they have to make one good decision: buying a good stock. But in fact, you have to make three good decisions: 1) buying a good stock 2) at the right time/price and 3) selling that stock at the right time/price. It’s like a parlay in gambling: if all three decisions aren’t good, you’ll lose money.

Most of the talking heads that discuss stocks are always talking about timing the market:

“Now’s the time to buys Tesla!” “Sell Walmart now!” (Have you noticed that they always seem to yell when they talk…?)

They’re trying to time the market. But history shows us (as evidence by this article) that unless you’re able to time travel, you’ll save yourself some heartache and some dough by having money in the stock market every day—good and bad—instead of trying to time the market. The time your money is in the market is much more important than timing the market.

I used to love watching infomercials. They were so captivating. My favorite tagline from an infomercial was from the Ronco Rotisserie Oven: “Just set it… and forget it!”

That’s how I invest most of my money in stocks. I don’t have time to be glued to the TV, my phone, or my brokerage app. I’m guessing you don’t either.

Which is good. Because if you’re willing to just “set it and forget it” with the money you have invested in the stock market, you’ll make a lot more money than you lose.

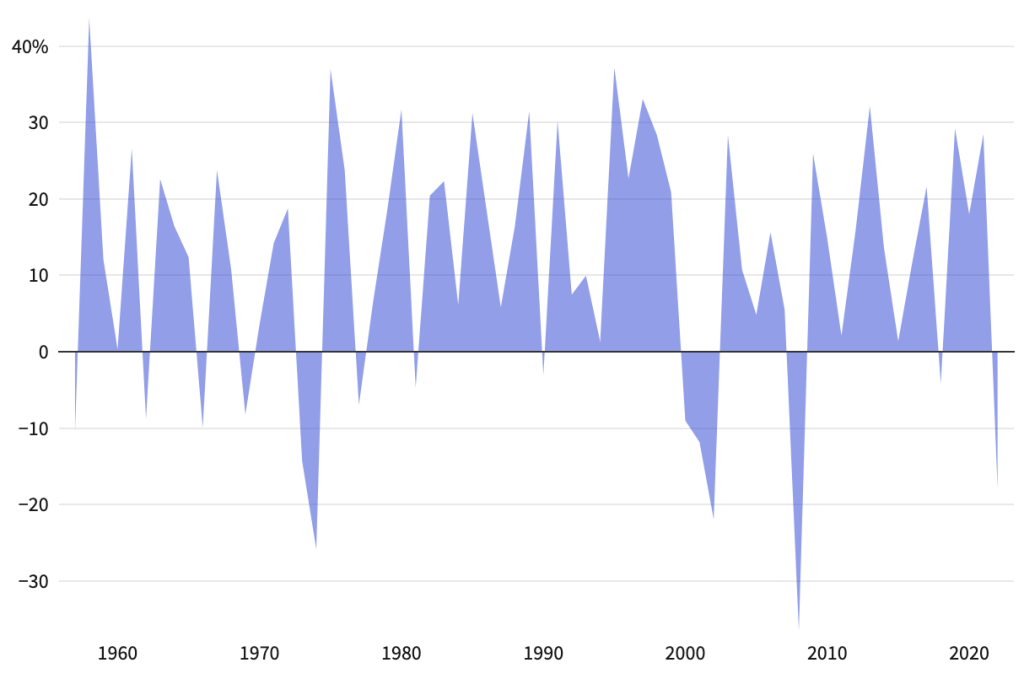

7. You don’t have to “beat the market.”

What if I told you that there was a stock that gave you this amount of returns each year since 1957?

I hope you’d buy it. And technically, it’s not a stock. It’s the S&P 500 (the 500 largest publicly traded companies in the US), which is what many people just refer to as “the market.”

Yet when I get fliers in the mail telling me to invest my money with So-and-So Investment Firm, they talk about “the market” as if it’s giving you junk returns.

“Don’t you want to beat the market?” “Last year, we returned our investors 2% more than the market!”

Since its inception in 1957, the S&P 500 has an annualized average return of around 10.26%. Over 10%! (I’m a bit more conservative: when I make calculations based on S&P 500 returns, I calculate using 8%)

Why do we talk about “the market” as if it’s bad to make what the market makes?

My philosophy is: invest in “the market” and make a lot of money doing so.

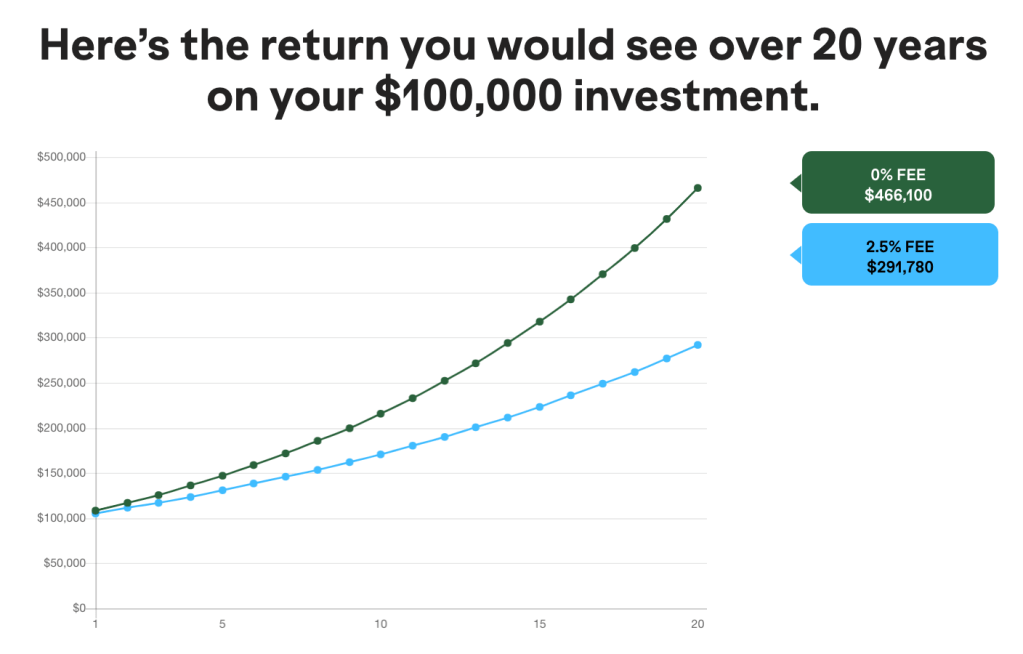

8. Fees kill returns.

Each time I have to choose a limited number of funds to put my money into (such as retirement or my HSA), the first thing I look at is the fee the fund charges.

Essentially, fees are what the fund or a financial planner charges you for investing your money. Which seems harmless. But if you have an average of $100,000 in a retirement fund (a very low amount for retirement) that charges a 2% fee (far from the highest fee I’ve seen), then in 40 years, you’ll have paid $80,000 just for them to invest your money. And frankly, it’s not a given that fund “beat the market.” So imagine how much money you’re giving to fees if you have an average of $500,000 or $1,000,000 (or more!) in a fund like that.

Many people also have financial advisors who charge fees on top of the funds they’re investing in. I have nothing against financial advisors and the work they do, but as an investor you need to know how much you’re paying for something you could do yourself (such as investing in a low-cost index fund).

Often, because individual investors don’t know how much they’re being charged, funds or financial advisors will charge exorbitant fees because they know that their investors won’t notice.

For a visual of how much fees can kill your returns, check out this chart (using an one-time initial investment of $100,000):

9. Take advantage of taxes.

Listen, taxes and the IRS scare me. I wish we didn’t have to deal with taxes and frankly, our tax system is ridiculously overcomplicated. But we do and until I’m elected president, we’ll keep having to pay taxes.

Because such a large amount of your finances are affected by taxes, it’s helpful to have a basic understanding of taxes and how they affect your money. Then, with that information, make intentional decisions.

Obviously each situation is different, but I’ll give two examples.

Last year, I began working full-time in June. Because I knew my income that year would be significantly lower than future years (likely lower than in retirement years, even), I put money in my Roth IRA and not my Traditional IRA so that I pay money at my current tax rate instead of my future tax rate. Understanding the difference between the two and my own financial picture helped me make that decision.

Additionally, after hearing ChooseFI talk about the triple tax benefits of a Health Savings Account (HSA), I’ve used our HSA as both a retirement vehicle and an emergency fund more than a health plan.

I’m no accountant or tax attorney (and have zero desire to be) but a little bit of asking questions, podcast listening, and Googling has gone a long way and made a significant impact on our finances.

10. Leave your heart out of it.

Investing is all about your brain and not your heart. Once you’re determined why you’re investing (see #1), then leave your heart out of it. When things get especially good or especially bad, your heart will want to override your brain.

Nearly all of my investing life, the stock market has been insanely good. It’s been hard to lose money in the stock market. But I know (and remind myself often) that a bear market (a drop of at least 20% from peak) is coming. When I make financial decisions now, I ask myself if I’ll stick with those decisions during a downturn. If not, then I don’t make that decision.

One of the biggest mistakes you can make in stock market investing is panic-selling in a downturn. Years or even decades of wise decisions can be overridden by one click of a “Sell” button.

If you know yourself well enough to know that you’ll hit the sell button during a drop of 30% (2020), 50% (2008), or even more, then there are plenty of other good, safer investments that might be better for you. And truly, there’s no shame in that.

One of the benefits of paying someone a fee to invest your money for you is that during downturns in the market, they can calm your anxieties and prevent panic-selling. And if they do that, they’ll be worth every penny you pay them.

In summary, the best thing you can do in investing is get to know yourself and build an investment portfolio that aligns with your own tendencies. Let your brain—not your heart—do that work for you.

At this point, some of you have been holding onto a question for quite a while. Your question goes something like this: Wait a second… what do money and faith have to do with each other? Why are you teaching a youth small group about money?

It’s a wonderful question and I appreciate the curiosity. Quite frankly, there are a lot of reasons. But two are especially important to me and are some of the motivating reasons why I’m co-leading this group.

First and foremost, because Jesus is Lord of everything. And everything includes our finances. Jesus doesn’t just want us to give Him lordship over just the “spiritual” parts of our lives (whatever that means to you). He wants us to give Him lordship over all parts of our lives: our attitudes, our careers, our relationships, and yes, even our money.

Because Jesus is Lord of our money but allows us to make decisions about how we earn, save, and spend our money, we become stewards of what is actually God’s. That’s why, before we do anything else with our money, we should approach it with prayer. That’s also why I don’t think I can give specific financial advice that is appropriate for everyone: because the way God wants you to use the money He has given you is different than the way God wants me to use the money He has given me. Therefore, we approach money with discernment and wisdom.

Secondly, money is a tool. In our first week together as a small group, one of my co-leaders asked a brilliant question: Did God invent money?

Simply, He didn’t. Money is a human invention. (We could make an argument that God inspired people to invent money, but I think you get my point.)

The reason humans invented money is to make commerce easier. So money, by its own invention, is a tool to something else. That “something else” can make a drastic difference in our lives. For you, is money a way of getting worth? Is money security? Is money opportunity? Is money a gift for others? Is money a vehicle that enables you to live into God’s calling on your life?

Money and the ways we use it can lead us closer to God, just like it can lead us away from God. As the church and as Christians, we would do well to talk about money and to establish a theology of money. In doing so, we’ll see Jesus as Lord of our money and our money as a way to welcome the Kingdom “on earth as it is in heaven.”

Leave a comment